What is the Corporate Sustainability Reporting Directive?

Corporate Sustainability Reporting Directive (CSRD) is the new EU sustainability directive adopted by the EU Parliament in November 2022. It means that more and more companies will have to monitor and report their impact on biodiversity. For those included in the directive, it is therefore important to understand and be able to interpret your company's impact on nature.

Background

The EU Biodiversity Strategy for 2030 is a comprehensive, ambitious and long-term plan to protect nature and reverse the degradation of ecosystems. The strategy aims to restore biodiversity in Europe by 2030. To achieve this goal, the EU's sustainability reporting has been revised and strengthened through the new CSRD directive. The requirements are extended to all large companies and all listed companies in the EU.

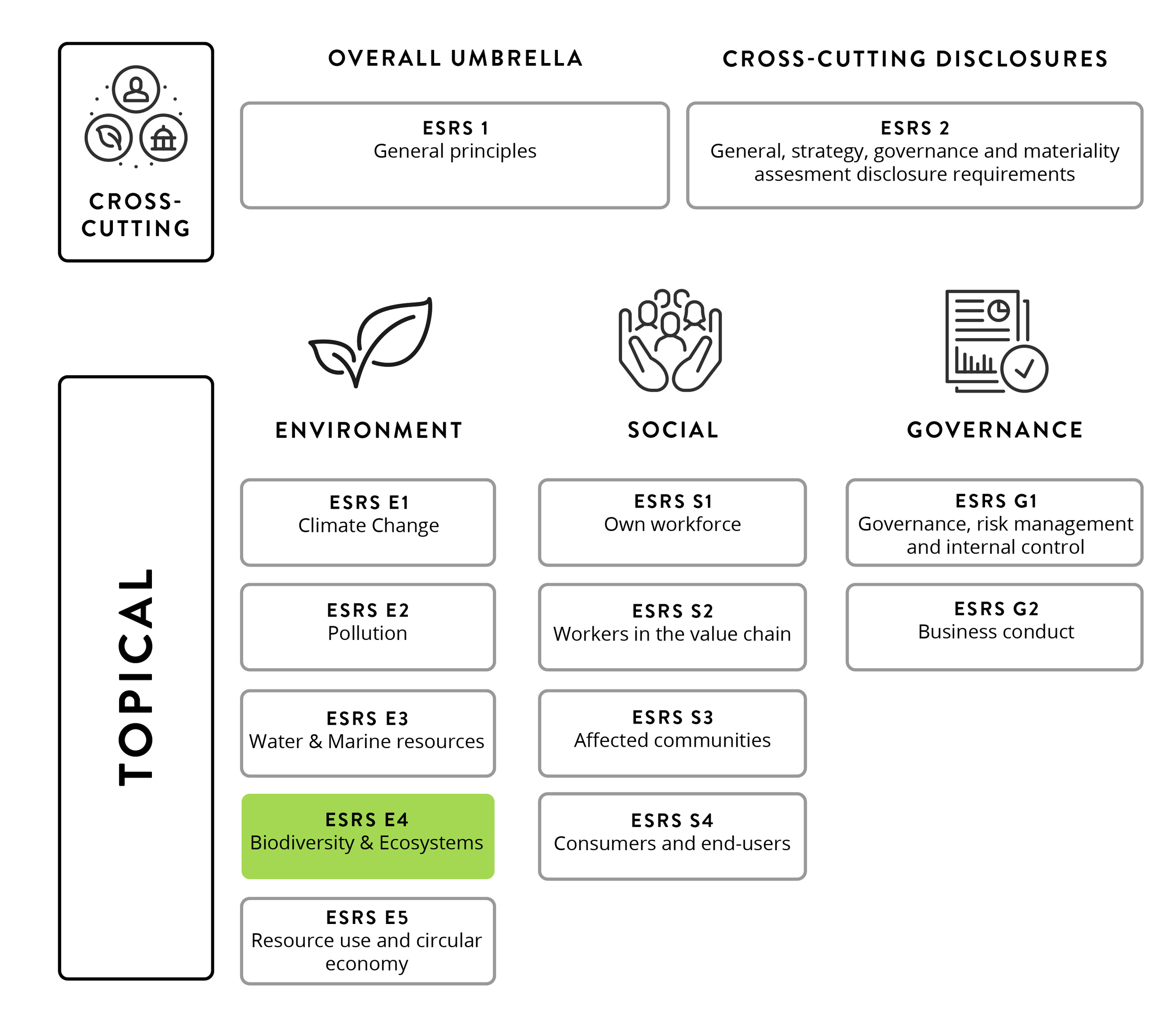

What is ESRS and how does it relate to biodiversity?

If CSRD is seen as the 'task' to be carried out in the context of sustainability reporting, the European Sustainability Reporting Standards (ESRS) are best explained as the 'tool' used to carry out the task. The ESRS are designed to help companies increase transparency and help specify the information to be disclosed such as environmental, social and governance issues.

The European Commission is working in the spring of 2023 to chisel out the draft ESRS that is available and expected to be adopted in June 2023. Biodiversity and ecosystems are specifically addressed in the ESRS E4.

Who is covered by the CSRD?

January 1, 2024 (reporting year 2025)

Companies already covered by the Non-Financial Reporting Directive.

Implies EU PIE i.e. >500 employees.

1 January 2025 (reporting year 2026)

Large companies currently not covered by the Non-Financial Reporting Directive.

250 employees 40 MEUR turnover, 20 MEUR BO.

January 1, 2026 (reporting year 2027)

Listed SMEs, small and non-complex credit institutions and captive insurance companies.

2028

Non-EU companies.

Over 150 MEUR turnover in the EU

- some information

An exemption will be possible for SMEs during a transitional period, meaning that they will be exempt from the application of the Directive until 2028.

CONTACT US FOR MORE INFORMATION AND ADVICE.

Helena Granborg, Head of Strategy

helena.granborg@ecogain.se

Tel: 010-405 90 30